The Bitcoin ETF Tipping Problem

The Bitcoin ETF Tipping Problem

With the "Tip Your Server" Era coming to Bitcoin, how does this even work?

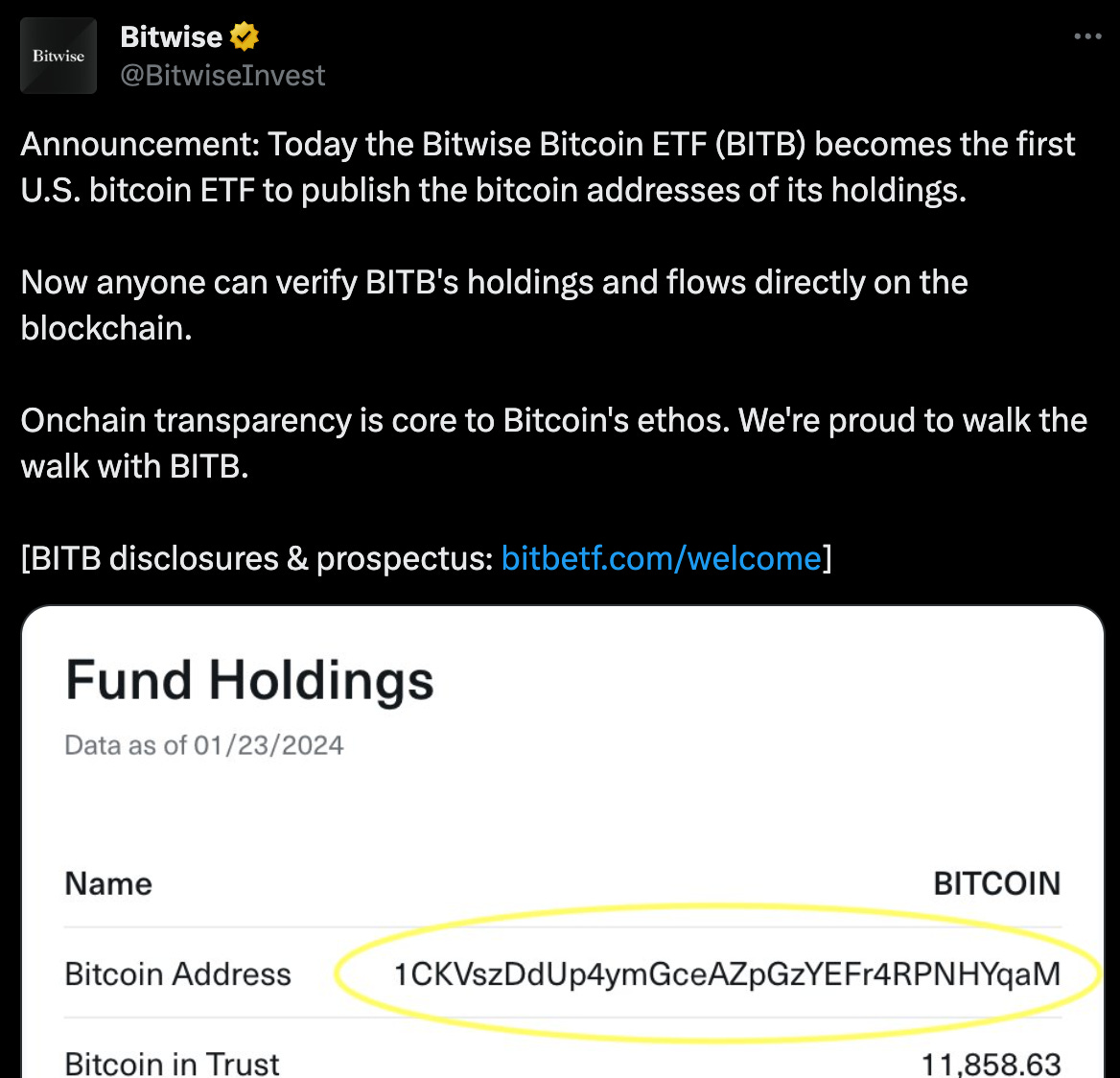

Matt Hougan of Bitwise and I first worked togehter in 1997 or so as part of “OpenFund - the World’s First Transparent Mutual Fund!” While we got shellacked, it’s not a surprise to see Matt and the team at Bitwise carrying the twin torches of “institutional quality” and “radical transparency,” which they refueled last week with this fun little move:

My first thought on seeing the wallet address out there was “OK, that’s clever… after all, it’s a one-way door, it doesn’t make anything less secure, and instantly solves the tired “theres no gold in the vault” insanity that’s plagued GLD.” (Which mindboggling is still going on to this day.)

What I hadn’t expected was that within hours, someone had just sent random bitcoin to this address:

Hong Kim is the CTO at bitwise, and I thought he did a good job of explaining things in a tweet, but since a bunch of folks asked, here’s my interpretation of the details and some of the fun implications.

The Big Questions

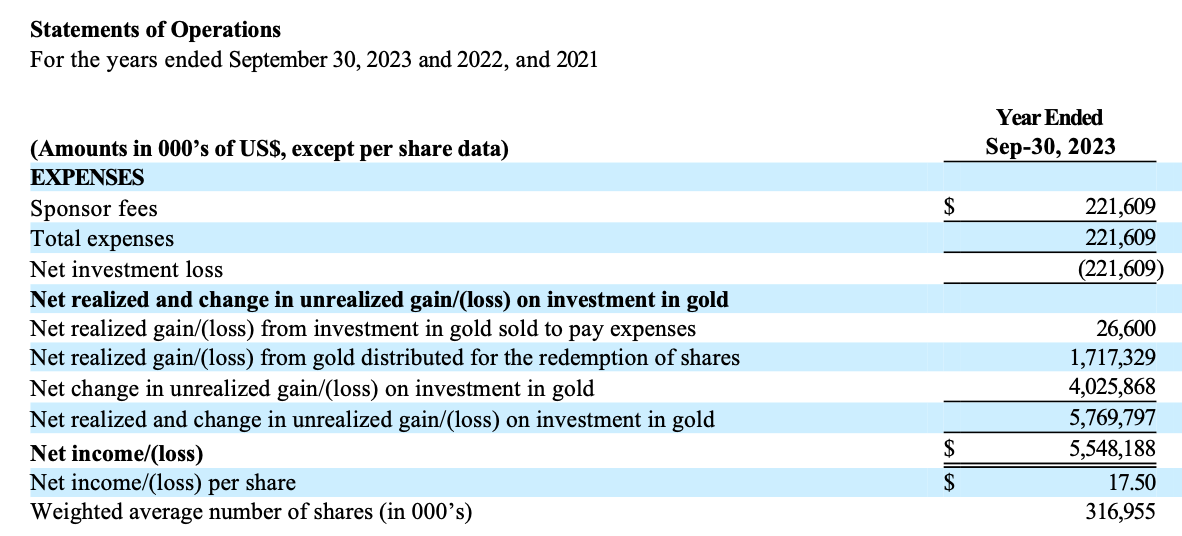

How the heck do you account for “donations”? Because I’m me, my immediate question was how this gets handled on the books of the fund. I’m pretty conversant in basic investment accounting principles, but not an actual CPA or lawyer or anything, but I stay up on GAAP changes (general accounting), the Uniform Principal and Interest Act (some Trust accounting) and the various interpretations for ETFs over the years, and I’m really pretty darn sure that the few hundred bucks showing up on the BITB books will have to be recorded as miscellaneous investment income on the funds Statement of Operations. Essentially adding a line we never see on, say, GLD’s annual:

Who Gets It? Because the Bitcoin ETFs are all essentially structured like GLD - Grantor Trusts that cleave to the “Widely Held Fixed Income Trust” IRS interpretations (could be wrong) - there’s not traditionally a dividend mechanism for distributing this “income” out to investors regularly, like there is in a more normal ‘40 Act fund. That’s only a problem to the extent that the amount of donations exceeds trust expenses, which, in a non-waiver period, seems exceptionally unlikely. Theoretically, someone could donate an enormous amount of BTC to the fund, and thus put the trust in the odd position of having to report income that they have not distributed (triggering a tax event for shareholders), or of having to actually distribute the income, which also seems insane and to my knowledge has never happened in Grantor-Trust structured ETPs. So: income, which will be offset by expenses.

Is this a threat? One wild idea I heard was that some bad actor could try and “poison” BITB or another ETF by routing a bunch of BTC through a sanctioned address and then sending it to the fund. The theory was that this would put the fund in some sort of illegal state, and tie it up with clawbacks and legal shenanigans. It’s an interesting idea (although I have no idea how one would do it or why one would want to), but if you dig into the Coinbase Custody agreements (or just their 2023 consent agreement with NY State) that’s just not how it works. As a big-boy institutional custodian, Coinbase siphons off anything from sanctioned addresses into a penalty box. As far as the Trust is concerned, no “bad” bitcoin ever goes anywhere near the fund — that’s for the Custodian to sort out with the Feds.

Is it in NAV? This one I am 100% sure of. Once Coinbase has allowed the donated BTC through to the custodial account without being flagged for sanctions, that BTC is absolutely an asset of the trust and will be in the very next NAV calculation. In this case, $400 isn’t going move the penny on NAV. But if someone just “gave” the trust $400 million or something? Sure. It’s in the NAV.

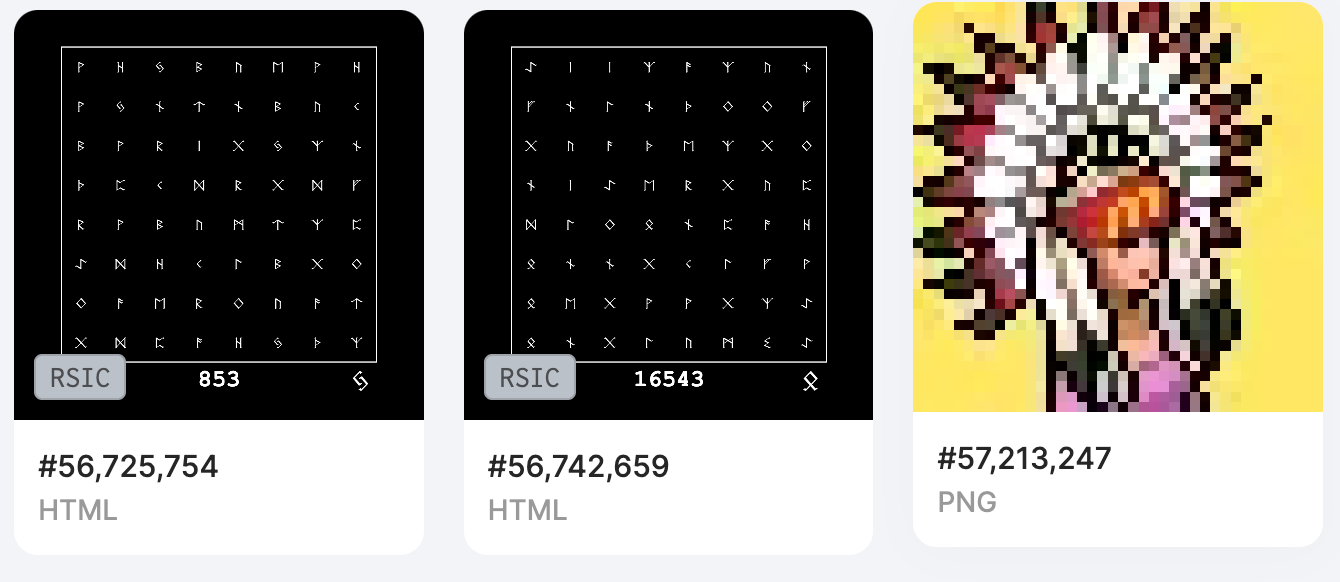

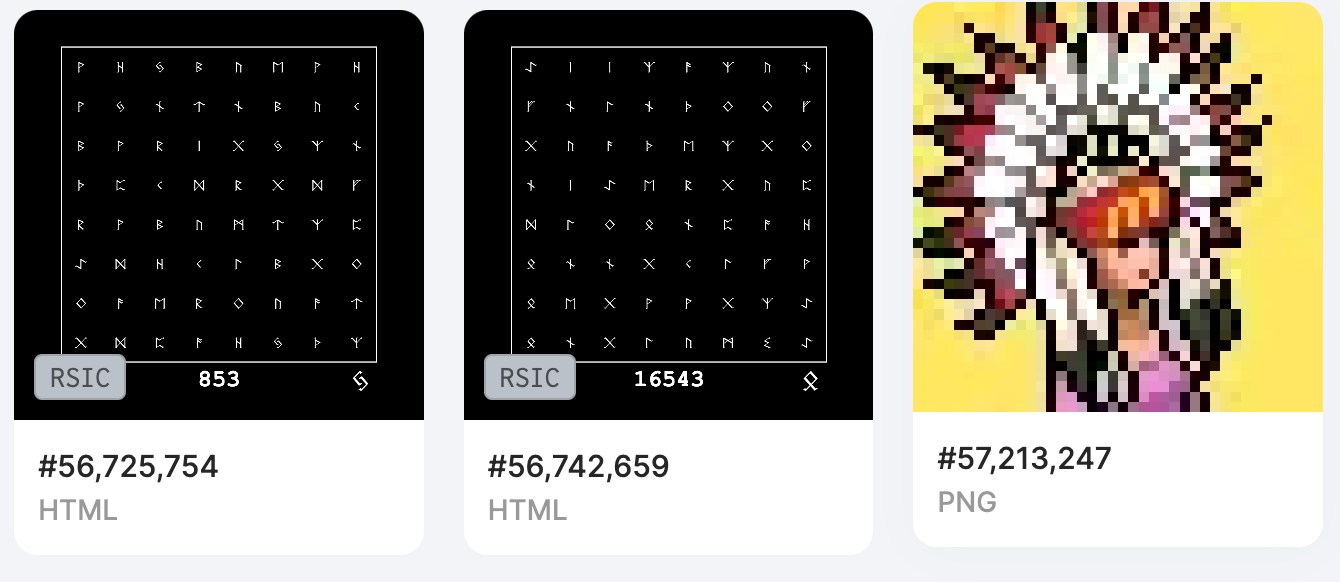

What about the NFTs!? Believe it or not, this is a thing. If you haven’t been paying attention to the NFT market, the new hotness for the last year has been “ordinals.” Every Satoshi (a 100 millionth of a Bitcoin) has a serial number from when it was minted. These days, you can embed some content in the process of minting a Satoshi, and that means you can make a crude, fully embedded NFT (not just a pointer to a JPG) - as long as the digital thing your inscribing on the Satoshi is less than 4MB. Turns out, a bunch of folks sent BITB some of them too

Here I feel like I’m on pretty solid ground in saying that any “value” someone might ascribe to “Ordinal 57,213,247” here beyond it’s value as Bitcoin (which it is), will be lost. In fact, because BITB is a grantor trust with a prospectus that could not state more clearly “Bitcoin will be the only digital asset held by the Trust.” They don’t “get” airdrops, or NFTs, or anything else. They get Bitcoin.

Does Any Of This Matter?

My friend Ben Hunt over at Epsilon Theory has been pretty negative about the BTC ETF phenomenon, and I myself wrote a whole thing on how the ETF does nothing to advance the BTC ethos other than create more scale potentially.

But here’s the thing: the very fact that I could even go down this rabbithole on a Saturday morning is proof that in fact it does matter that we’ve created these first little footbridges between the BIG IDEA of Bitcoin and DeFi, and the staid old world of TradFi. I think “how do you deal unexpected value from digital assets in a legal structure like a grantor trust ETF” is an interesting conversation, if only for it’s poignancy in in illustrating the bizarre, byzantine and entirely made up system of modern finance.

The technology and possibility of Crypto have fascinated me since the dawn. Here in the mid-day of crypto, I continue to believe the actual, most important, most interesting dialog is about how the possible interacts with the now. Our legal system (particularly the U.S. legal system) is still just starting to wrestle with the most important parts of the possible — in Crypto, in AI, in Robotics, in communications.

Weirdness like the above is an important step in that wrestling match. My take away is that it’s cool that we do have answers — pretty good ones — to all of the above questions, partly because the ETF corner of the legal system is finely, finely honed and has been through the flames for 30 years. It’s just as imaginary as every other social construct, but in this case, it’s a pretty useful imaginary social construct.

We can lament “financializing” crypto, but that ship sailed a long time ago. I for one plan to learn from the bridge-building (and bridge-maintainance,) not root for collapse.

(I could be wrong about some of the above, in which case, drop me a comment! I learn more from being wrong than being right!)

This is all very helpful for understanding the "how" donating Bitcoin to an ETF can happen. I'm still lost on the "why," though. What would possess someone to just... give money to an ETF without expecting shares in return? If you wanted to be philanthropic for crypto causes, surely there are other ways than by handing an ETF your loose change? What am I missing?

Great write up on this fast moving corner of the ETF world.